Then, if σdaily = 0.01, the annualized volatility is. The monthly volatility (i.e., T = 1/12 of a year or P = 252/12 = 21 trading days) would be. The formulas used above to convert returns or volatility measures from one time period to another assume a particular underlying model or process.

Is Historical volatility Annualized?

However, historical volatility is an annualized figure, so to convert the daily standard deviation calculated above into a usable metric, it must be multiplied by an annualization factor based on the period used.

How do you calculate monthly return volatility?

To calculate the monthly volatility, you must take the square-root of the variance. The result will be the standard deviation of the stock’s monthly returns, and this is the most commonly used parameter when financial professionals talk about risk and volatility.

What does annualized volatility tell you?

To annualize volatility, it’s necessary to measure volatility over a shorter period of time and extrapolate it over the course of a year. Volatility is a measure of the variance of returns over a period of time. In order to figure out what the variance of returns is, the daily returns must first be calculated.

What is stock historical volatility?

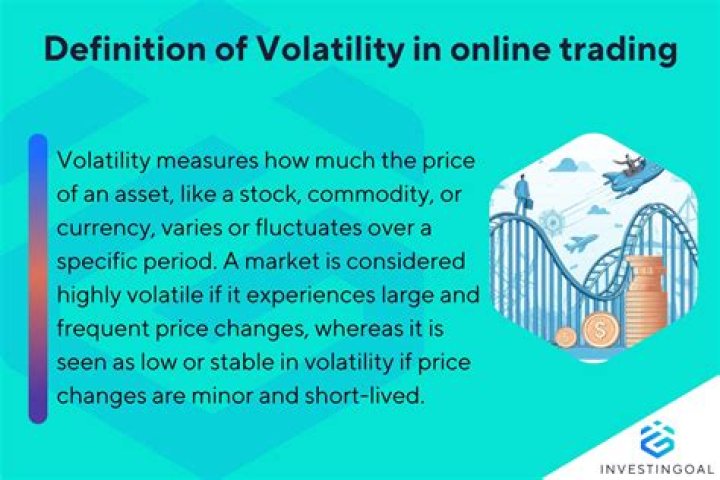

Historical volatility (HV) is a statistical measure of the dispersion of returns for a given security or market index over a given period of time. Generally, this measure is calculated by determining the average deviation from the average price of a financial instrument in the given time period.

What is a good volatility percentage?

Defining market volatility comes with a surprisingly low bar: any time the market moves up and down by one percentage point or more over a sustained period, it’s technically considered a volatile market. That said, the implied volatility for the average stock is around 15%.

How do you present volatility in annualized terms?

To present this volatility in annualized terms, we simply need to multiply our daily standard deviation by the square root of 252. This assumes there are 252 trading days in a given year. The formula for square root in Excel is =SQRT ().

What is annualized total return in finance?

Annualized Total Return. Loading the player… An annualized total return is the geometric average amount of money earned by an investment each year over a given time period. It is calculated as a geometric average to show what an investor would earn over a period of time if the annual return was compounded.

What is the annualized volatility of the monthly standard deviation?

Suppose we have monthly returns for an asset. From these returns, we calculate the monthly standard deviation, and find it to be 5% per month. However, we need the annual standard deviation for our analysis. We can calculate the annual standard deviation as follows The annualized volatility equals 17.32%.

How to calculate volatility in trading?

The volatility can be calculated either using the standard deviation or the variance of the security or stock. The formula for daily volatility is computed by finding out the square root of the variance of a daily stock price. Further, the annualized volatility formula is calculated by multiplying the daily volatility by a square root of 252.